DSWM Quarterly: Q4 2025

Investing Insights

We have used two words frequently this year to describe the markets, consistent and resilient. We can use them again to describe the 4th quarter, since positive momentum for the markets which started early in 2025 was maintained through the end of the year. When you describe a market as consistent, the usual assumption might be that not much occurred in the world to move markets. That was not the case this quarter or this year, however the market maintained the same resiliency to headline risk it has exhibited all year. During the 4th quarter, the market endured the longest U.S. government shutdown in history, rising investor concerns over the durability of tech stock valuations, and wavering job data to only name a few headlines.

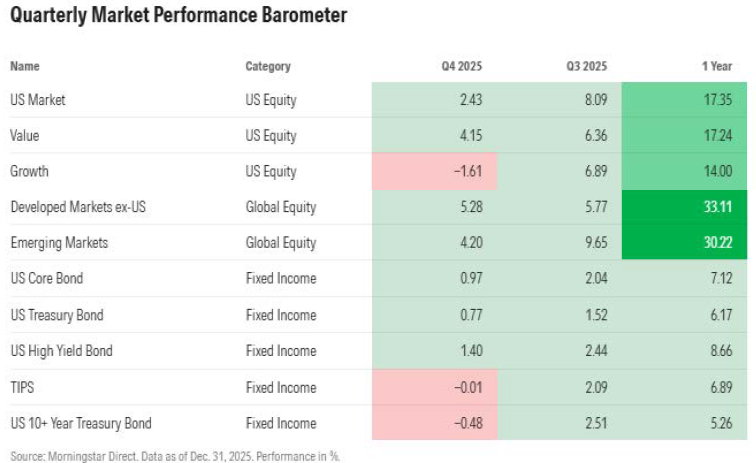

In the U.S., large cap equities were up 2.40% for quarter and more importantly, we saw a broadening of gains beyond the tech sector. During the 4th quarter investors began to express concerns regarding spending on artificial intelligence in the tech sector, leading to volatility in growth stocks. However, value stocks bolstered the U.S. equity market and offset the pullback in growth stocks. For the year, 7 stocks represented slightly over half of the S&P 500’s gains in 2025: NVIDIA, Alphabet, Microsoft, Broadcom, JPMorgan Chase, Palantir Technologies and Meta Platforms. These 7 stocks punched well above their weight, as they represent just 25% of the S&P 500’s market capitalization for 2025, but they contributed 52% of the index’s total return for the year. All but one company are obvious direct benefactors of the expanding implementation of artificial intelligence (AI) and the potential future benefits. The one company outside of the tech sector is banking behemoth JPMorgan Chase. Some analysts view JPMorgan Chase being included in the wave of investor AI exuberance as a sign that the market could start shifting from rewarding only the creators/implementors (tech companies) to companies using the technology. The theory is that after companies implement some of the new AI technologies, they will see expanding efficiencies within their businesses, broadening the benefit of AI beyond just technology companies. Small cap U.S. stocks outperformed U.S. large cap stocks for the second quarter in a row. A few factors that pushed small cap stocks ahead in the second half of the year were increasing flexibility around tariff policies, expectations for lower interest rates, and the U.S. consumers’ unwavering strength despite elevated prices.

Throughout 2025, the bond market was completely focused on when the Federal Reserve would resume cutting rates. The spotlight on the Fed’s rate policy grew consistently stronger throughout the year as opinions from outside the Fed policy makers grew louder and louder. Answers came in the second half of the year as Fed policy makers voted to lower rates three times, two of which came during the 4th quarter. At times, the easing rate environment gave way to elevated volatility, but the result was that most areas of the bond market finished with positive returns. The three rate cuts pushed short-term yields down, which further steepened the yield curve bringing it a bit closer to what might be considered a “normalized” curve. For economists, a normal yield curve (an upward sloping curve) entering 2026 is a positive sign, as it is viewed as an indicator of economic stability and potential for growth.

International equities shined in 2025, posting the best year for stocks outside of the U.S. since 2017. During the fourth quarter international equites’ returns outpaced U.S. equities at a nearly 2-1 one pace. There are a couple factors driving those returns, the first being the starting point for international equities. While equities outside of the U.S. have posted positive returns since the widespread market selloff in 2022, they have not recovered at nearly the magnitude of U.S. equities. That left many foreign markets to be viewed as an attractive valuation for investors to start the year. The other factor is the weakness in the U.S. dollar throughout the year. The U.S. dollar had been on an upward trajectory all the way back to 2011, but in 2025 the greenback shed over 8% of its value against other major currencies. This results in returns earned in foreign currencies to incur an additional gain when those returns are converted back to U.S. dollars. Emerging markets also had a strong end to the year, China being the main contributor as their tech sector continues to get closer to the U.S. in the AI technology race. In fact, technology has become one of the biggest sectors in emerging markets equities, in addition to China, other Asian countries like South Korea and Taiwan are hubs for key AI components hardware manufacturing.

Looking forward to 2026, the combination of lower inflation, lower interest rates and roughly two percent or better GDP growth that are often required for continued stock market gains leads us to think that duplicating 2025 performance in 2026 may be a high hurdle. Additionally, the typical volatility associated with midterm election years could also take its toll on the market. To put the current bull market in perspective, since 1945, the S&P 500 has delivered above-average gains for three or more consecutive years on five other occasions (not counting this cycle), including one streak that ran for four years and another for five. If we rely on history as our gauge, a fourth year of above average returns, while not unprecedented, is rare.

If the 2020s have taught us anything so far, it’s that life is unpredictable. The first half of the decade was consumed by a pandemic, wars in Europe and the Middle East, evolving global trade dynamics, and political unrest. The second half could be determined by the emergence of generative AI. Or not. Since we do not know what to expect from 2026 or the rest of the 2020s, we prepare your portfolio for the unknown ahead through diversified portfolio construction, monitoring, and disciplined long-term investing so the focus is maintained on your long-term goals. We also continue to carefully monitor gains in client accounts, trim back equity positions to capture gains as well as maintain asset allocations at the agreed upon targets.

As we move into a new year, we would like to express our extreme gratitude for the trust you place in everyone here at Droms Strauss each day. Happy New Year!