DSWM Quarterly: Q3 2025

Investing Insights

Over the last quarter, U.S. and global markets posted strong gains, maintaining consistent upward momentum across most major asset classes. This was a change from the first two quarters of 2025 where uncertainties, primarily in global trade policies, led to tumultuous periods and varying returns between the U.S., developed countries, and emerging markets. In the U.S., the combination of stable inflation data, the perception of easing trade tensions, and strong corporate earnings contributed to investors’ optimism. The Federal Reserve’s decision to shift to a more expansionary monetary policy by resuming rate cuts also generated positive sentiments here in the U.S.

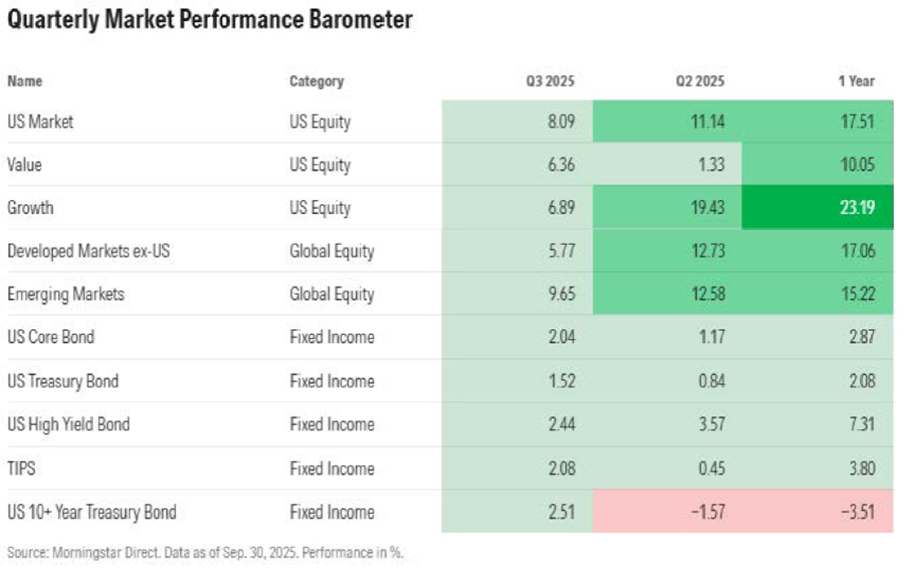

In the U.S., the S&P 500 was up 7.4%, the Nasdaq Composite up 11.2%, and the Russell 2000 small-cap index climbed 12.4% for the quarter. The bullishness on Artificial Intelligence (AI) applications continued to fuel U.S. large cap growth stocks. However, in a shift from last quarter, the breadth of stocks contributing to returns for the S&P 500 increased as U.S. large cap value stocks nearly matched the returns of large cap growth stocks. Also notable for the quarter is the performance of small caps, as they outperformed large caps and hit a new all-time high (as measured by the Russell 2000) for the first time since 2021. Much of the optimism around small cap equities stems from smaller companies perceived outsized benefit, compared to larger companies, from lower rate environments since much of their growth is dependent on debt financing.

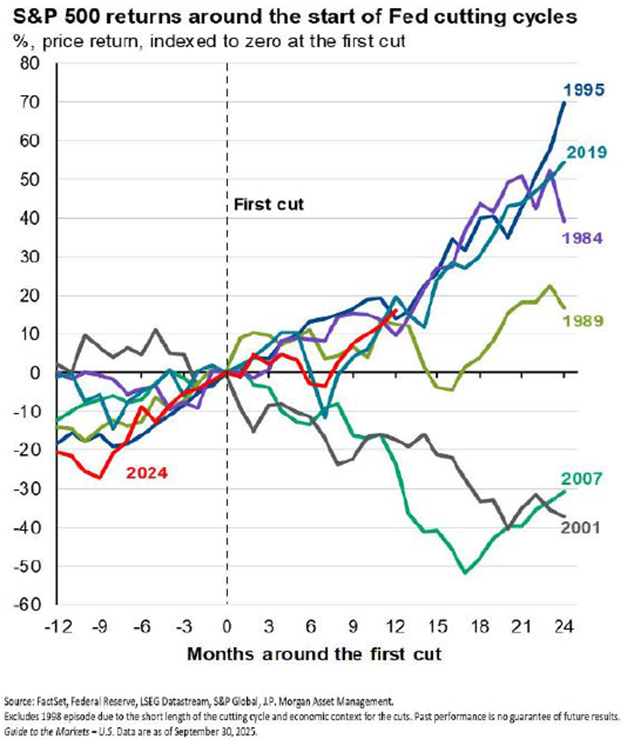

What we find most interesting about the third quarter markets is the lack of volatility during the quarter. If we look at the S&P 500 over the past 15 years, on average the index trades close to 10% below its peak at some point during the quarter (if we extend to 1980, the average increases to hitting almost 15% below its peak during each quarter which is not surprising as that period includes, 2000 dot-com bubble burst and the 2008-2009 Great Recession). This past quarter, the furthest the S&P 500 traded from its peak was roughly 2.4%, which from the standpoint of volatility marks one of the mildest quarters for the index on record. Looking forward, much attention will be paid to the Federal Reserve’s upcoming rate decisions and whether they will meet the market expectations of cuts at both their October and December meetings. As the chart shows, in general, rate cutting cycles have shown mixed results from U.S. equities. That said, it should be noted the 2001 and 2007 cycles both were during extremely volatile conditions in equity markets, so taking that into account it can be said in more stable conditions rate cutting cycles are generally favorable for U.S. equites.

Broadly, fixed income assets posted positive returns for the quarter as yields were pushed down by investors anticipating the Federal Reserve to resume easing interest rates. The first rate cut in almost a year came in September, with the indication that subsequent cuts are expected but their pace is dependent on future economic data. The market expectations of two more rate cuts in 2025, point to weakening labor market data combined with relatively subdued inflation which is defying tariff-driven price pressures. Outside of the U.S., most developed countries saw yields push higher. The upward pressure on many developed countries’ yields stems from a still uncertain economic impact from U.S. trade policy along with many countries increasing government spending.

International developed market equities added a third straight quarter of positive returns, albeit at a slower pace than the first half of the year. The easing concerns of trade tensions, along with stimulative monetary policy made for favorable conditions in most developed markets. We saw positive returns from the Eurozone, UK, and Japan. Emerging markets also performed well as they benefited from shifting global trade dynamics as well as a weaker U.S. dollar. The one laggard amongst the emerging market countries was India, which during the quarter faced renewed trade frictions with the U.S. related to its dealings with Russia.

While this past quarter was a rare occurrence of positive trajectories across nearly all asset classes, we know that it’s impossible for volatility to disappear forever and we believe it is unlikely that reduced volatility has anything more than a very short life. It is impossible to anticipate when volatility is going to return but we know that it will. The financial media will lead you to believe that the “bubble” is going to burst tomorrow and investors need to act quickly, not surprising since that is what gets our attention. Although the media might sensationalize market risks, we would not suggest that the risks do not exist. For example, equity valuations continue to hit new highs but if some of the AI applications hit a road bump, those valuations could pull back. From an economic standpoint, recent data shows the labor market is beginning to weaken. A weakening labor market coupled with inflation, which is no longer dropping, and the lingering uncertainties around the impact of tariffs all create investment risks. The point we are trying to make is there are always risks, particularly over the short-term, and reacting to them can cause you to miss out on the returns if we stay invested.

While delivering positive returns for our clients is what we strive to do every day, the team at Droms Strauss does not take a vacation because the market is going up. We are monitoring your portfolio, trimming the appreciated positions, and rebalancing back to your targeted allocation so your portfolio is well situated when volatility does return.

Droms Strauss Wealth Management

www.droms-strauss.com

(314) 862-9100

For information purposes only. Opinions expressed herein are solely those of Droms Strauss Wealth Management, unless otherwise specifically cited. Material presented is believed to be from reliable sources, but no representations are made by our firm as to another parties' informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant, or legal counsel prior to implementation. Past performance may not be indicative of future results. Indexes are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns.