DSWM Quarterly: Q1 2026

Investing Insights

The first quarter of 2026 served as a good reminder that market conditions can change quickly. After 2025 delivered historically low volatility and strong returns across most areas of the market, 2026 started the same way. However, as the quarter went on investors’ enthusiasm began to wane and volatility returned to the markets after being practically absent for over a year. The emergence of A.I. has propelled technology stocks and in turn the overall market since 2022, however uncertainty about the disruption A.I. adoption could cause in various industries, along with the labor market, began to weigh on equities. At the end of February came the geopolitical shock with the start of the war with Iran. The conflict ignited a sharp rise in oil prices and renewed inflation concerns which further deepened the selloff in global equity markets.

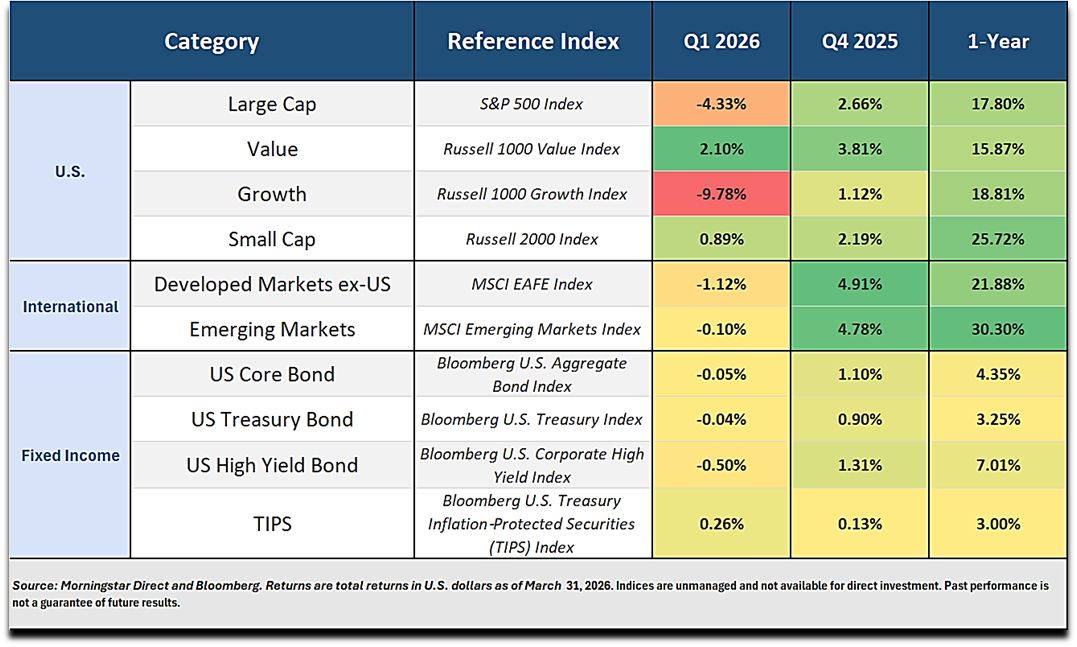

Over the quarter, the S&P 500® dropped roughly 9% from January highs, to finish down 4.33%. While U.S. equities notched their worst quarter since 2022 the consensus among Wall Street analysts is not raising alarms. They point to U.S. corporations which are still in a strong position. Their opinion of corporate America was reinforced by fourth quarter earnings which showed a 14% year-over-year growth. Along with the U.S. economy, that showed relative strength for the quarter, with steady economic growth and stable consumer spending. Another healthy signal for the U.S. equity market is the continued broadening of equity returns beyond the mega-cap growth stocks, as exemplified by the disparity in the U.S. large cap value to growth returns for the quarter. U.S. small cap stocks continued to outpace large caps, attributed to investor optimism that smaller companies will benefit from the expected lower rate environment and attractive current valuations after years of below average returns. As was the case with U.S. large cap stocks during the first quarter, investors favored small cap value stocks to growth.

Fixed income markets faced a challenging first quarter, as early‑year optimism gave way to rising volatility driven by the war in Iran. After posting slightly above average returns in 2025, bond markets finished the first quarter flat to modestly negative, with income offset by rising yields and spreads widening late in the period. The Bloomberg U.S. Aggregate Bond Index ended the quarter slightly negative, reflecting these cross‑currents. The rise in inflationary pressures driven by surging energy prices and other global supply chain disruptions complicates the Federal Reserve’s policy outlook. While market participants began the year expecting multiple interest rate cuts, those expectations were pushed out as the quarter progressed. The Federal Reserve held policy rates steady throughout the quarter, signaling a cautious approach amid heightened uncertainty around inflation and global growth conditions.

International equities were relatively flat to slightly negative in places but showed more resiliency for the quarter compared to U.S. equities overall. As in U.S. markets, international companies saw much of their year-to-date gains erased as March wore on. European markets declined as elevated energy costs and geopolitical proximity to the Middle East conflict raised concerns about economic growth and inflation persistence. Higher natural gas prices weighed on the region, prompting investors to reassess earnings outlooks, particularly in energy‑sensitive industries. In contrast, Japanese equities were a notable outperformer during the quarter. A combination of yen weakness, continued corporate reforms, and supportive domestic policy developments helped offset global risk‑off pressures. Emerging market equities delivered relatively stronger performance compared with developed markets, though results varied widely by country and region. Markets with exposure to technology, manufacturing, and commodities held up better early in the quarter, while energy importers faced increasing pressure as oil prices surged.

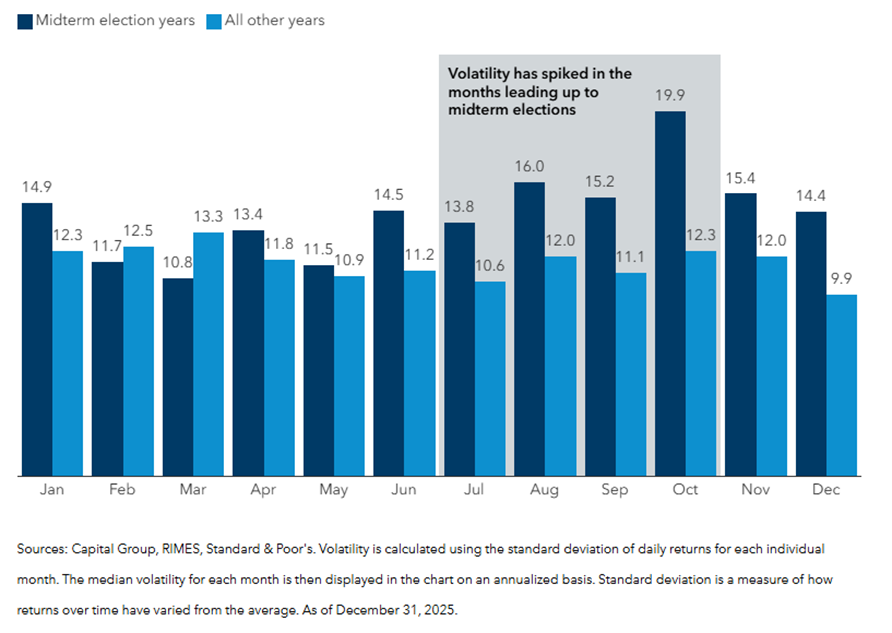

Looking ahead, the specific catalysts driving volatility may evolve; uncertainties around geopolitics, inflation dynamics, and central bank policy remain in the forefront. In addition, history shows that markets often grow uneasy leading up to mid-term elections as uncertainty around policy direction begins weighing on investor sentiment. The chart compares volatility in midterm election years to all other years. The impact on volatility is clear in the months leading up with a dramatic variance in October, just before U.S. voters head to the polls. There is a silver lining which lies beyond November: once political visibility improves, U.S. markets historically have delivered above-average returns the following year (since 1950, the average return on the S&P 500® in the year following a midterm election has been 15.4%). However, every cycle is different, and elections are just one of many factors influencing short-term market returns.

Periods such as this highlight the value of maintaining a long‑term perspective and the importance of recognizing that market volatility is a normal feature of investing. As markets continue to adjust to shifting economic and policy conditions, we focus on maintaining diversified portfolios with appropriate risk exposures to help navigate an environment where volatility may persist.