DSWM Quarterly: Q1 2023

Investing Insights

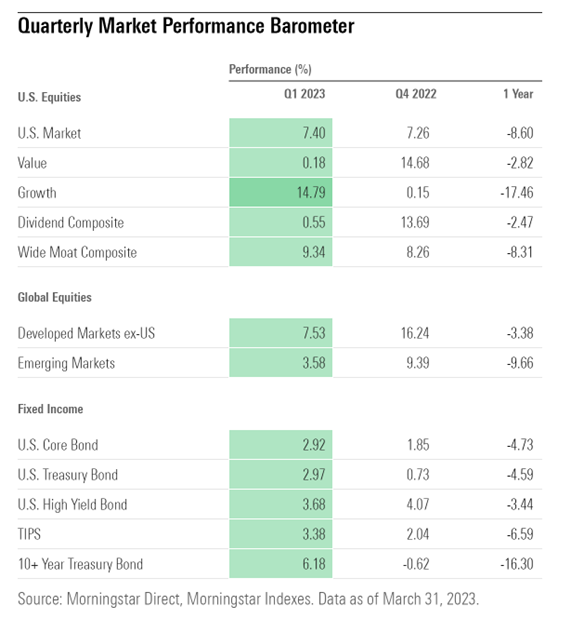

Why hasn’t anyone noticed? The first quarter of 2023 offered strong returns across most asset classes, and no one seemed to notice. Why? Perhaps it is because that investors around the world were still coming to terms with their 2022 year-end statements. Or, maybe it was because the ride this quarter was like a roller coaster – we all know that we remember the downhill rush more than the smooth uphill climb. In January we experienced a rapid climb in the S&P but then, from early February to mid-March the sudden dive almost to where we started the beginning of the year. Could this be why we haven’t noticed the steady climb since mid-March? The S&P 500 was up 7.09% this past quarter but we would bet that many of us are still thinking about 2022 when the S&P 500 was down 18.11%; a similar fact pattern holds true for bonds, where the Bloomberg U.S. Aggregate Bond index was up 2.96% this past quarter (that’s a bond return of almost one percent per month!) but we are still thinking about the negative return for bonds of 13.01% in 2022. Are we guilty of focusing more on the past than the future? Maybe a better reason to explain investor’s indifference to a strong start for 2023 is an abundance of caution as we try to figure out what we think the Fed is going to do with continuing the almost monthly interest rate increases or, is there going to be a recession later this year.

The Federal Reserve’s rate hiking cycle celebrated its first birthday on March 15th, and it is an unwritten rule that monetary policy changes normally take at least a year to show their effects. The markets performed well through January as signs that inflation was easing along with a resilient job market gave some indications to investors that the rate hikes were effectively pulling inflation down. However, celebrating a Fed victory against inflation would be premature. Rising prices are still a concern and are a key factor driving markets and could cause turbulence ahead. Unfortunately, another part of when a rate hiking cycle starts taking effect is it has historically “broken” something. In the early 80’s, a rate hiking cycle successfully reigned in inflation but pushed the economy into recession and set off the Latin American debt crisis. A rate hiking cycle in the late 90’s took the blame for a selloff in equities which burst the dot-com bubble, resulting in a recession. And rate hikes from 2004 to 2006, were one of many variables that popped the housing bubble leading us into the Great Recession. In February we saw this rate hiking cycle “break” something with the failures of Silicon Valley Bank, Signature Bank and Credit Suisse. In the case of Silicon Valley Bank and Signature Bank, as rates rose over the past year long term fixed income holdings on the banks’ balance sheets suffered large losses. Once the news of the losses spread, depositors at both banks looked to quickly withdraw their funds and the banks had no reserves to fund the withdrawal requests. Regulators immediately put in place facilities to bolster the banking system; an invaluable lesson learned from the 2008 Financial Crisis was that swift action can keep a problem amongst a few financial institutions from bringing down an overall healthy financial system. The swift actions in February restored confidence in the banking system and to this point has kept the situation to two (U.S.) bank failures. While rising rates can be said to have “broken” these banks, the real cause was poor risk management combined with a largely uninsured deposit base.

This history lesson is not meant to imply that a recession is certain. There is still hope for an economic “soft landing” as we are seeing steadily decreasing year-over-year inflation numbers, resilient economic data, and the labor market continues to be strong. This time, perhaps the Fed really can deliver an economic soft landing, whereby the economy slows but avoids a painful recession. At the March meeting of the Federal Reserve, policy makers signaled that they may be very close to ending the current rate hike campaign. That, combined with no additional large bank failures, eased concern about a global bank crisis and the S&P demonstrated its resilience with a rally that began mid-March and has continued through mid-April. Despite all the uncertainty, continuing inflation concerns, future economic growth, and what we hope is the end of the banking crisis, markets have been resilient since hitting their lows in October 2022.

Looking forward there are still plenty of potential headwinds for markets globally. Investors are facing the highest interest rates in decades, the worst geopolitical tensions in years, and potential areas of fragility in the economic system have been exposed by the recent bank failures. However, it cannot be ignored that U.S. economic fundamentals and U.S. corporate earnings have been resilient through the first quarter, which are both real long-term drivers of market returns. Focusing on that last point helps us keep a long-term perspective to our investment strategy and not get deterred by the financial news headline of the day.

While we can not predict how long volatile markets will be with us, we can make sure our portfolios are prepared for volatile times. That started with building a well-planned long-term strategy which includes a diversified portfolio and priority towards risk/return management. Your plan and portfolio evolves as your goals and life change, NOT with the headline of the day. We recognize the risks facing both the markets and the economy, and we are committed to helping you successfully navigate this challenging investment environment. That said, we will remain diligent and stick to the long-term plan, as we’ve worked with you to establish a unique, personal allocation target based on your financial position, risk tolerance, and investment timeline.

We remain vigilant towards risks to portfolios and the economy, and we thank you for your ongoing confidence and trust.

Please do not hesitate to contact us with any questions, comments, or to schedule a portfolio/financial plan review.

DISCLOSURE: The opinions voiced in this material are for general information and nothing in this material should be construed as investment advice offered or a recommendation of any particular investment, security, portfolio of securities, transaction or investment strategy by Droms Strauss Wealth Management. No chart, graph, or other figure provided should be used to determine which securities to buy, sell or hold. You should speak with your own financial professional before making any investment decisions.

Past performance is not indicative of future results. The market and economic data are historical and is no guarantee of future results. All indices are unmanaged and may not be invested in directly. The information in this report has been prepared from data believed to be reliable as of the date of this material, but no representation is being made as to its accuracy and completeness. These disclosures cannot and do not list every conceivable factor that may affect the results of any investment or investment strategy. Risks will arise, and an investor must be willing and able to accept those risks, including the loss of principal.

Certain statements contained herein are statements of future expectations and other forward-looking statements that are based on opinions and assumptions that involve known and unknown risks and uncertainties that would cause actual results, performance or events to differ materially from those expressed or implied in such statements.

Droms Strauss Wealth Management is a Securities and Exchange Commission (SEC) registered investment adviser. Registration does not imply a certain level of skill or training.